Transforming Personal Finance with Cash Flow Banking and Life Insurance

Table of Contents

- Understanding Cash Flow Banking

- The Role of Life Insurance

- Benefits of Cash Flow Banking

- Potential Risks and Considerations

- Steps to Implement Cash Flow Banking

- Real-Life Applications

- Conclusion

Managing personal finances has evolved beyond just saving and investing in traditional accounts. One powerful strategy gaining attention is cash flow banking, particularly when it is integrated with life insurance. This innovative approach enables individuals to effectively leverage the cash value of a life insurance policy, providing access to capital, potential tax advantages, and a more flexible personal banking system. By visiting https://privatebankingstrategies.com/cash-flow-banking-life-insurance/, individuals can find opportunities to enhance their financial security and pursue independent wealth-building strategies. At its core, cash flow banking is about using the features of permanent life insurance to unlock liquidity and control. Instead of relying solely on commercial banks for loans and financing, policyholders access the cash value in their insurance policies through low-interest policy loans. This can help maximize savings potential, provide greater stability, and maintain financial flexibility in times of need. Understanding these mechanics is central to making the most of the strategy while balancing the associated risks. As more people seek creative ways to strengthen their financial futures, it is important to evaluate how cash flow banking works in real-world scenarios. This system is not only useful for individuals but can also benefit families, entrepreneurs, and business owners by reducing dependency on outside lenders and supporting long-term wealth growth.

- Cash flow banking leverages the cash value in life insurance to build a private banking system.

- Key benefits include tax advantages, uninterrupted compound growth, and financial autonomy.

- Understanding the required commitments and risks is essential before adopting this strategy.

Understanding Cash Flow Banking

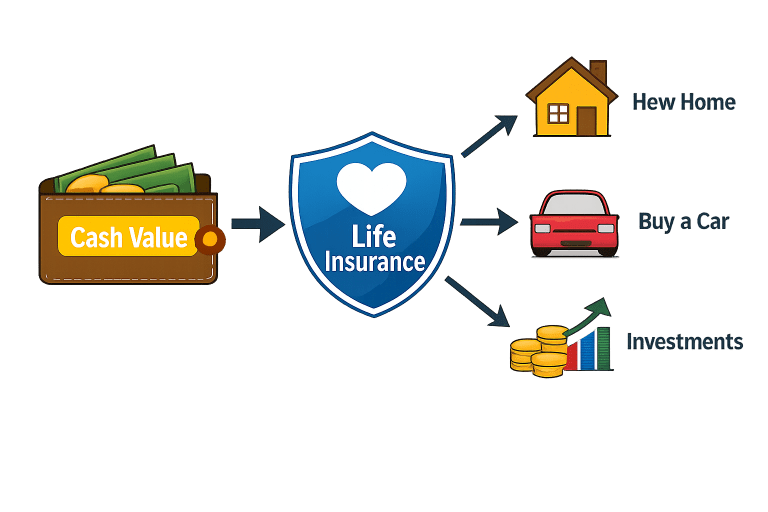

Cash flow banking is a sophisticated personal finance strategy that involves the overfunding of a permanent life insurance policy, such as whole life. The goal is to rapidly build up the policy’s cash value, which acts like a personal bank that you control. Once the policy holds sufficient cash value, the owner can take out policy loans for any purpose, from investments to emergencies, while the policy’s cash value continues to grow. These policy loans do not require standard credit checks or lengthy approval processes, making them an attractive option for those wanting quick access to liquidity.

The Role of Life Insurance

Whole life insurance is the preferred vehicle for cash flow banking because it offers guaranteed cash value accumulation and lifelong coverage. Over time, the premiums paid into a whole life policy build up a cash reserve, called the cash value, which grows tax-deferred. Policyholders can borrow against this value at competitive interest rates. Unlike traditional bank loans, policy loans come with no credit checks and flexible repayment schedules. However, unpaid policy loans and accrued interest can decrease the death benefit paid out to beneficiaries. This means careful management and regular review of loan balances and repayments are essential.

Benefits of Cash Flow Banking

- Tax Advantages: Loans from a life insurance policy are not taxed as income, and the growth in the cash value is tax-deferred. This provides potential tax savings over the life of the policy.

- Uninterrupted Compound Growth: One unique advantage is that the cash value in your policy continues to earn dividends and interest even when you borrow against it. This means your money can grow as if it were never withdrawn, provided premiums are kept current.

- Financial Control: Policy loans put the policyholder in charge, offering immediate access to funds for investments, purchases, or emergencies without the stringent requirements of banks.

These advantages can help build a strong personal financial foundation, especially for those who want to diversify beyond conventional banking and investment approaches.

Potential Risks and Considerations

While there are significant benefits, adopting a cash flow banking strategy has some important hurdles and considerations:

- Policy Costs: Whole life insurance is more expensive than term life due to higher, permanent premiums designed to accumulate cash value. For some, this can be financially straining if not budgeted correctly.

- Loan Interest: Borrowing from your policy carries interest costs. If unattended, interest can deplete the cash value or, if premiums and interest payments are not maintained, eventually cause the policy to lapse.

- Policy Lapse: Failing to repay policy loans or keep up premiums could result in your policy lapsing, which means losing both the insurance coverage and any accumulated cash value. This can also trigger tax consequences on outstanding loan balances.

To mitigate these risks, it is recommended to revisit one’s overall financial plan with a trusted advisor and keep a disciplined approach to managing payments and loans. For further guidance, Forbes offers a well-balanced look at these factors.

Steps to Implement Cash Flow Banking

- Consult a Financial Advisor: Start by discussing your financial goals and current situation with a licensed financial professional experienced in cash flow banking strategies.

- Select the Right Policy: Carefully compare whole life insurance policies from leading insurers, focusing on those with strong dividend histories, flexible options, and transparent fees.

- Overfund the Policy: To maximize cash value growth, contribute premiums above the base requirement as allowed by IRS guidelines. This accelerates the buildup of usable cash value.

- Utilize Policy Loans Wisely: Use policy loans strategically for income-generating investments or major life expenses. Ensure you have a repayment plan to protect the policy’s integrity and long-term value.

Real-Life Applications

This strategy is particularly attractive to business owners and entrepreneurs. For example, consider a contractor who needs new equipment and borrows from their policy’s cash value. This approach streamlines the process by bypassing bank approvals while the cash value continues to grow. The contractor repays the loan on flexible terms, maintaining liquidity for future opportunities. Similarly, families may use policy loans for tuition, medical expenses, or to bridge income gaps, all while keeping their financial engine compounding in the background.

Conclusion

Cash flow banking, when paired with permanent life insurance, creates a compelling model for personal and family finance. By leveraging the cash value of a policy, individuals improve their liquidity, enjoy potential tax savings, and reduce their dependence on traditional banking systems. Success with this approach depends on understanding its structure, the discipline to manage the policy responsibly, and ongoing consultation with financial professionals. Adopting cash flow banking could be a key step in achieving greater financial autonomy and lasting wealth.